Bernie’s Blog

What’s this FTX Thing Anyway and Should I Be Worried?

Hello! It’s Bradley, Marci’s eldest here again (with some light editing from my mom) hoping to shed some light on what FTX is, why it is collapsing, and what that means for your portfolio (spoiler alert, hopefully, not much).

First things first, what is FTX? FTX is (was) a cryptocurrency exchange. This is, very simply, a place where people can buy and sell cryptocurrency (for more on what cryptocurrency is, see the February 28th, 2021 Bernie’s Blog post about Bitcoin). It works similarly to how our Ameritrade/Schwab accounts work. An investor puts money into an account there, and then buys and sells Bitcoin, or other cryptocurrencies (including FTT, the cryptocurrency started by FTX), just as we buy and sell other securities in our Ameritrade and Schwab accounts.

Now, what happened? Like brokerage accounts and banks, FTX did not actually hold all of its deposits in cash. There’s nothing necessarily wrong with this; we all know that banks make loans with much of their deposits (they are required to hold approximately 10% of their deposits as reserves at any given point in time to accommodate customer’s withdrawals), and Ameritrade does similarly with money in money market accounts. However, unlike banks or brokerages, FTX held its reserves in its own cryptocurrency FTT and had lent much of its customer’s deposits to its sister trading company Alameda Research. Because cryptocurrencies are highly volatile, this means that the value of its reserves could very rapidly diminish. And diminish they did, as the value of FTT has plummeted this year along with most other cryptocurrencies. When customers of FTX heard that FTX was in trouble, many tried to withdraw their deposits at the same time, leading to an old-fashioned bank run. This caused FTX to have to declare bankruptcy, which is where we are now.

What caused FTX’s downfall? Several things:

- The CEO of FTX, Sam Bankman-Fried was less than transparent to his customers about the risks of trading cryptocurrency and then used his customers’ money to fund his other businesses. This is against the law, and he could be looking at significant consequences if found guilty.

- Cryptocurrency is highly volatile, and essentially unregulated. Unlike stocks and bonds, it has no inherent value, and cryptocurrency exchanges are not protected by the same regulations that banks are. (For example, bank deposits are insured by the FDIC, protecting against bank runs).

How does this affect you, and what can we learn from this? Marci here..

- Because we do not recommend cryptocurrency for clients, any direct impact of FTX’s collapse should be very small. As of yet, cryptocurrency is quite separate from traditional stock and bond markets, so any spillover should be insignificant.

- LFS is a fiduciary which means that we are legally obligated to act in your best interests. That includes only recommending investments that are appropriate to your particular situation and which we can explain to you (including the risks).

- As always, if an investment idea sounds too good to be true, it very likely is.

It’s Not Too Late to Buy I Bonds!

For those of you that haven’t yet gotten around to buying an I Bond yet this year or if you haven’t bought your full $10K allotment, there is some good news…. You can still do before October 31 and get the 9.62% interest rate for the first six months. After November 1, the interest rate on new I Bonds (and those that have been held for 6 months) will go down – probably to the 6% range. That’s still not bad, but it’s not 9.62%!

The process is a bit clunky, but we have some tools to help make it a little easier for you to do or we can do it with you on the phone. Just let us know if you need help.

Refer back to Bernie’s Blog of Jun 11 for all the details or just keep reading… I have copied the text from the June 11 Bernie’s Blog post below:

Most of you have probably heard of I Bonds by now, either from us or from your favorite media personality. Let’s talk about what these actually are and who can benefit. Spoiler alert, if you are reading this, you can most likely benefit!

What is an I Bond and how does it differ from a TIP?

I Bonds are inflation adjusted 30-year U.S. savings bonds. The inflation adjustment happens twice per year and is based on the Consumer Price Index (CPI). From now until October, the annual variable interest rate (coupon) is 9.62%. No really, 9.62%. These are U.S. treasuries so 100% safe, the actual value of the bond does not fluctuate, and the interest is added to the bond value every six months. These bonds are also tax efficient because the interest is only subject to Federal income taxes and only when the bond matures or is sold.

Since many of you own TIPs (Treasury Inflation Adjusted Notes), you are undoubtedly asking yourself if these are different. The answer is that they are different in some important ways, but they complement each other perfectly. First of all, for a TIP, the coupon rate stays constant throughout the bond life but the principal amount on which the coupon rate is applied is adjusted twice per year, based on the CPI. TIPs are great for long term inflation protection, and we like them, especially in IRA’s because the TIP interest and inflation adjustment are taxed every year at your full tax rate. There is also no dollar limit on TIP purchases, and you can own TIPs in your Ameritrade accounts and sell them at any time.

Are I Bonds too good to be true?

I Bonds are not too good to be true BUT there are some important limitations:

- Each person can only purchase $10K in electronic I Bonds each year. There are no income or age limitations. They can also be purchased for children (and grandchildren!). Minors can own I Bonds but they can’t have their own Treasurydirect account.

- These must be purchased via the Treasurydirect website and held at the Treasury. The account set up and purchase is a bit of a clunky process, but we can help you. I Bonds cannot be owned in brokerage accounts or IRA’s or your bank.

- These bonds must be held for at least 12 months. If they are sold between 1 and 5 years, there is an interest penalty of three months. I Bonds will earn interest for up to 30 years, but obviously when inflation moderates, they will become less attractive.

- Each I Bond can have only one beneficiary.

Are I Bonds for me and how do I get started?

In general, I Bonds are for you, as long as you have enough cash remaining in your cash reserve after the purchase to sustain you for at least one year, and preferably 5 years. We will discuss individually with you this quarter but feel free to call if you want to discuss now. Obviously, the sooner you purchase, the more interest you will earn!

As I said above, the process is a little clunky with a lot of information, multiple passcodes/security questions and double factor authentication required. Because these are not held at Ameritrade, our normal “do for you with your approval” process does not work. We have developed a form for you to use on your own so that you have all the info you need in front of you when you begin the process, and we are also happy to undertake a “do with you” process to open the account and buy these I Bonds.

Happy to answer questions and to help!

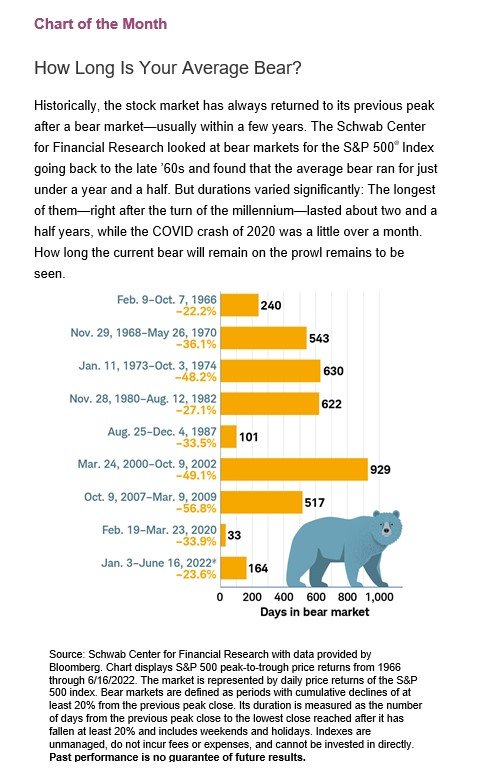

How Long Do Bear Markets Usually Last?

We are asking ourselves this question so you might be too. The answer is “too long” of course.

We like this chart from Schwab which provides a historical perspective, which of course means nothing about the current situation – except that bear markets have ended 100% of the time they have happened in the past!

Two More Inflation Fighting Ideas

After you have purchased I Bonds (you can still do, and we can help!) we want to share two more ideas!

Stock up on stamps and run low on gasoline. We are…

What’s Going on With Transition from TD Ameritrade to Schwab?

We ask ourselves this question nearly every day so some of you are probably ready for an update too.

As a reminder, in 2019 Schwab announced that it was acquiring TD Ameritrade. The deal actually closed in October 2020 with the implementation timeline expected to be 30 to 36 months from that point. As you may remember, the news at that time was that both companies would continue to operate as largely separate entities until the transition was complete. Schwab is now confirming that the actual conversion is expected to be on schedule – sometime between April and September 2023.

What have we experienced so far?

Both Schwab and Ameritrade realize how complicated this transition is – for them, for us and for you. They are committed to minimizing the disruption for all of us while delivering a customer experience and platform which is better than what we have now. Both companies are committed to getting the conversion right the first time – for advisors and for clients. All good to hear. Thus far, we see great commitment, communication, and lots of testing, but we recognize the heavy lifting ahead.

As many of you know, we signed up for the Schwab “jumpstart” program which allows TD Ameritrade advisors an opportunity to get an earlier look at and experience using the Schwab platform. We did this so we will not be on our Day 1 while you are on your Day 1! We moved a handful of our personal accounts (lots of paperwork to do!), absorbed a few onboarding sessions and then jumped into “learning by doing.” See attached photo of Marci “learning by doing.” You will be happy to know to know that at least so far, we haven’t messed anything up badly enough that we couldn’t undo and redo – although there has been a fair amount of undoing and redoing. Not a problem.

There are a few things we have already seen which we really like:

- The client interface (called Schwab Alliance) which will replace TD Advisor Client is easy to use and the mobile experience is much improved. The security has been upgraded and some features which were not available on TD Ameritrade’s mobile platform will be available on Schwab’s. That’s good.

- Schwab doesn’t allow DocuSign as much as TDA does (not sure THAT is such a bad thing) but they do have an electronic signature process via Schwab Alliance which is easy to use and doesn’t require clients to remember the car they owned in 1967. This is good too!

- The phone support has been excellent – and we have needed it.

What have we been told will happen, but we have not seen yet?

- There will be no need for any paperwork for account transfer from TD Ameritrade to Schwab unless accounts are moved before the official transition date. Spoiler alert – we will want to continue to build our Schwab experience in the next year so we will want to move some additional client accounts but we will do the paperwork as usual so you will not have to do. Let us know if you want to be early adopter.

- Existing account and advisor authorizations which are on the Ameritrade platform (trading authorization, fee deductions, option trading, electronic statement delivery, etc) will be carried over to Schwab.

- Most account history will be transferred over. We also have all of your LFS quarterly updates since you joined our LFS family.

- Some of the beneficiary info will have to be updated after the transfer.

- There are likely hundreds of questions we haven’t even though of yet!

What do we need to do with you over the next 9 to 15 months? We will take the lead here!

- Data clean-up. Since most information will be directly transferred, we can all help by ensuring that what we transfer is up to date. That includes mailing and email addresses, phone numbers etc. We will also want to close any account which are not funded. We can always re-open those at Schwab if they are needed.

- Where possible, we want to update any automatic transfer instructions between your Ameritrade accounts and your checking account to “pull” from Ameritrade rather than “push” from Bank of America (for example). These transfer instructions will then automatically migrate to Schwab. If that can’t happen, it’s fine – we will just have to redo those after the conversion with your new Schwab account info.

- We have been told that this transition will be much easier if clients have an active Advisor Client account at Ameritrade. We know that some of you do not use Advisor Client but for those of you that do, we will want to ensure that your access is up to date.

Let us know what questions you have so far! We have time to get this work done with you way ahead of the actual transition.

I Bonds… I Bonds… I Bonds… I Bonds

Most of you have probably heard of I Bonds by now, either from us or from your favorite media personality. Let’s talk about what these actually are and who can benefit. Spoiler alert, if you are reading this, you can most likely benefit!

What is an I Bond and how does it differ from a TIP?

I Bonds are inflation adjusted 30-year U.S. savings bonds. The inflation adjustment happens twice per year and is based on the Consumer Price Index (CPI). From now until October, the annual variable interest rate (coupon) is 9.62%. No really, 9.62%. These are U.S. treasuries so 100% safe, the actual value of the bond does not fluctuate, and the interest is added to the bond value every six months. These bonds are also tax efficient because the interest is only subject to Federal income taxes and only when the bond matures or is sold.

Since many of you own TIPs (Treasury Inflation Adjusted Notes), you are undoubtedly asking yourself if these are different. The answer is that they are different in some important ways, but they complement each other perfectly. First of all, for a TIP, the coupon rate stays constant throughout the bond life but the principal amount on which the coupon rate is applied is adjusted twice per year, based on the CPI. TIPs are great for long term inflation protection, and we like them, especially in IRA’s because the TIP interest and inflation adjustment are taxed every year at your full tax rate. There is also no dollar limit on TIP purchases, and you can own TIPs in your Ameritrade accounts and sell them at any time.

Are I Bonds too good to be true?

I Bonds are not too good to be true BUT there are some important limitations:

- Each person can only purchase $10K in electronic I Bonds each year. There are no income or age limitations. They can also be purchased for children (and grandchildren!). Minors can own I Bonds but they can’t have their own Treasurydirect account.

- These must be purchased via the Treasurydirect website and held at the Treasury. The account set up and purchase is a bit of a clunky process, but we can help you. I Bonds cannot be owned in brokerage accounts or IRA’s or your bank.

- These bonds must be held for at least 12 months. If they are sold between 1 and 5 years, there is an interest penalty of three months. I Bonds will earn interest for up to 30 years, but obviously when inflation moderates, they will become less attractive.

- Each I Bond can have only one beneficiary.

Are I Bonds for me and how do I get started?

In general, I Bonds are for you, as long as you have enough cash remaining in your cash reserve after the purchase to sustain you for at least one year, and preferably 5 years. We will discuss individually with you this quarter but feel free to call if you want to discuss now. Obviously, the sooner you purchase, the more interest you will earn!

As I said above, the process is a little clunky with a lot of information, multiple passcodes/security questions and double factor authentication required. Because these are not held at Ameritrade, our normal “do for you with your approval” process does not work. We have developed a form for you to use on your own so that you have all the info you need in front of you when you begin the process, and we are also happy to undertake a “do with you” process to open the account and buy these I Bonds.

Happy to answer questions and to help!