Bernie’s Blog

Big News from the Linders

Dear Family, Friends and LFS Clients,

We are happy to share our BIG NEWS:

We are moving to Atlanta!

Move date: Depends on which of us you ask, but likely in February New Address: 2051 Peachtree Rd NE

Atlanta, GA 30309

Apt 909Phone: 828-692-0061 (home) – same

828-279-5247 (Bernie cell) – same

828-708-2973 (Toby cell) – sameEmail: bernd.linder@linderfinancial.com – same

tobyleelinder@gmail.com – sameWine: yes. Available now. Bernie and Toby

January “TO DO” List from LFS

Happy New Year again! As we begin 2023, we have our usual list of things for us to do together. The good news for you is that not all of these action items will apply to you!

First of all, RMDs: As usual, your required minimum distribution (RMD) is based on the year-end balance in your traditional or beneficiary IRA’s. Because the market was less than stellar in 2022, your 2023 RMD is likely less than your 2022 requirement. Your RMDs can be fulfilled in any combination of cash, shares transferred to an after-tax cash account or a tax-advantaged charitable contribution. We will help you get this done, either as one distribution or as periodic withdrawals. Your federal and state taxes are usually withheld. Traditional Roth IRAs have no RMD requirements while Beneficiary Roth’s do, although no taxes are due. The age at which RMDs must be initiated has increased but as always, there are rules around this change. If this change impacts you, we will tell you and help you figure out what to do.

Secondly, contribution limits for all types of retirement accounts have been increased for 2023:

- 401K or 403B: Employee contribution is being increased from $20,500 to $22,500. If you are over 50, your contribution has increased from $27,000 to $30,000. You need to make this change directly with your plan administrator, but we can help you figure out how to adjust your monthly contribution. As always, this contribution can be in any combination of Roth 401K/403B and traditional 401K/403B if your plan offers both. There are no income limits for a Roth 401K.

- Traditional or Roth IRA’s contribution limit is being increased from $6,000 to $6,500. If you are over 50, your contribution is being increased from $7,000 to $7,500.

- Roth IRA’s: Earned income eligibility has been increased:

- Modified Adjusted Gross Income (MAGI) for full contribution increased from$129,000 to $138,000 for single taxpayers

- Modified Adjusted Gross Income (MAGI) for full contribution increased from$204,000 to $218,000 for married, filing jointly taxpayers

- There are partial contributions allowed above these limits. Call us for details.

- SEP or SIMPLE IRA’s: Call us

- You can still make 2022 IRA contributions until April 17, 2023. Special paperwork is required to ensure the contribution is applied to the correct year. Call us.

Next, if you have your cash reserve fully funded (in a high yield savings account please) and have extra coins under your sofa cushions, you can now buy another I Bond for $10,000. The annual interest rate is 6.89% for the first six months for any I Bonds issued by May 30. At that time, the rate will be adjusted again. We can help you purchase I Bonds whether or not you bought one in 2022. Lots of rules here just like last time. Call us.

This is enough for now. We are here to help so feel free to call, text or email. Or drop by!

What’s this FTX Thing Anyway and Should I Be Worried?

Hello! It’s Bradley, Marci’s eldest here again (with some light editing from my mom) hoping to shed some light on what FTX is, why it is collapsing, and what that means for your portfolio (spoiler alert, hopefully, not much).

First things first, what is FTX? FTX is (was) a cryptocurrency exchange. This is, very simply, a place where people can buy and sell cryptocurrency (for more on what cryptocurrency is, see the February 28th, 2021 Bernie’s Blog post about Bitcoin). It works similarly to how our Ameritrade/Schwab accounts work. An investor puts money into an account there, and then buys and sells Bitcoin, or other cryptocurrencies (including FTT, the cryptocurrency started by FTX), just as we buy and sell other securities in our Ameritrade and Schwab accounts.

Now, what happened? Like brokerage accounts and banks, FTX did not actually hold all of its deposits in cash. There’s nothing necessarily wrong with this; we all know that banks make loans with much of their deposits (they are required to hold approximately 10% of their deposits as reserves at any given point in time to accommodate customer’s withdrawals), and Ameritrade does similarly with money in money market accounts. However, unlike banks or brokerages, FTX held its reserves in its own cryptocurrency FTT and had lent much of its customer’s deposits to its sister trading company Alameda Research. Because cryptocurrencies are highly volatile, this means that the value of its reserves could very rapidly diminish. And diminish they did, as the value of FTT has plummeted this year along with most other cryptocurrencies. When customers of FTX heard that FTX was in trouble, many tried to withdraw their deposits at the same time, leading to an old-fashioned bank run. This caused FTX to have to declare bankruptcy, which is where we are now.

What caused FTX’s downfall? Several things:

- The CEO of FTX, Sam Bankman-Fried was less than transparent to his customers about the risks of trading cryptocurrency and then used his customers’ money to fund his other businesses. This is against the law, and he could be looking at significant consequences if found guilty.

- Cryptocurrency is highly volatile, and essentially unregulated. Unlike stocks and bonds, it has no inherent value, and cryptocurrency exchanges are not protected by the same regulations that banks are. (For example, bank deposits are insured by the FDIC, protecting against bank runs).

How does this affect you, and what can we learn from this? Marci here..

- Because we do not recommend cryptocurrency for clients, any direct impact of FTX’s collapse should be very small. As of yet, cryptocurrency is quite separate from traditional stock and bond markets, so any spillover should be insignificant.

- LFS is a fiduciary which means that we are legally obligated to act in your best interests. That includes only recommending investments that are appropriate to your particular situation and which we can explain to you (including the risks).

- As always, if an investment idea sounds too good to be true, it very likely is.

It’s Not Too Late to Buy I Bonds!

For those of you that haven’t yet gotten around to buying an I Bond yet this year or if you haven’t bought your full $10K allotment, there is some good news…. You can still do before October 31 and get the 9.62% interest rate for the first six months. After November 1, the interest rate on new I Bonds (and those that have been held for 6 months) will go down – probably to the 6% range. That’s still not bad, but it’s not 9.62%!

The process is a bit clunky, but we have some tools to help make it a little easier for you to do or we can do it with you on the phone. Just let us know if you need help.

Refer back to Bernie’s Blog of Jun 11 for all the details or just keep reading… I have copied the text from the June 11 Bernie’s Blog post below:

Most of you have probably heard of I Bonds by now, either from us or from your favorite media personality. Let’s talk about what these actually are and who can benefit. Spoiler alert, if you are reading this, you can most likely benefit!

What is an I Bond and how does it differ from a TIP?

I Bonds are inflation adjusted 30-year U.S. savings bonds. The inflation adjustment happens twice per year and is based on the Consumer Price Index (CPI). From now until October, the annual variable interest rate (coupon) is 9.62%. No really, 9.62%. These are U.S. treasuries so 100% safe, the actual value of the bond does not fluctuate, and the interest is added to the bond value every six months. These bonds are also tax efficient because the interest is only subject to Federal income taxes and only when the bond matures or is sold.

Since many of you own TIPs (Treasury Inflation Adjusted Notes), you are undoubtedly asking yourself if these are different. The answer is that they are different in some important ways, but they complement each other perfectly. First of all, for a TIP, the coupon rate stays constant throughout the bond life but the principal amount on which the coupon rate is applied is adjusted twice per year, based on the CPI. TIPs are great for long term inflation protection, and we like them, especially in IRA’s because the TIP interest and inflation adjustment are taxed every year at your full tax rate. There is also no dollar limit on TIP purchases, and you can own TIPs in your Ameritrade accounts and sell them at any time.

Are I Bonds too good to be true?

I Bonds are not too good to be true BUT there are some important limitations:

- Each person can only purchase $10K in electronic I Bonds each year. There are no income or age limitations. They can also be purchased for children (and grandchildren!). Minors can own I Bonds but they can’t have their own Treasurydirect account.

- These must be purchased via the Treasurydirect website and held at the Treasury. The account set up and purchase is a bit of a clunky process, but we can help you. I Bonds cannot be owned in brokerage accounts or IRA’s or your bank.

- These bonds must be held for at least 12 months. If they are sold between 1 and 5 years, there is an interest penalty of three months. I Bonds will earn interest for up to 30 years, but obviously when inflation moderates, they will become less attractive.

- Each I Bond can have only one beneficiary.

Are I Bonds for me and how do I get started?

In general, I Bonds are for you, as long as you have enough cash remaining in your cash reserve after the purchase to sustain you for at least one year, and preferably 5 years. We will discuss individually with you this quarter but feel free to call if you want to discuss now. Obviously, the sooner you purchase, the more interest you will earn!

As I said above, the process is a little clunky with a lot of information, multiple passcodes/security questions and double factor authentication required. Because these are not held at Ameritrade, our normal “do for you with your approval” process does not work. We have developed a form for you to use on your own so that you have all the info you need in front of you when you begin the process, and we are also happy to undertake a “do with you” process to open the account and buy these I Bonds.

Happy to answer questions and to help!

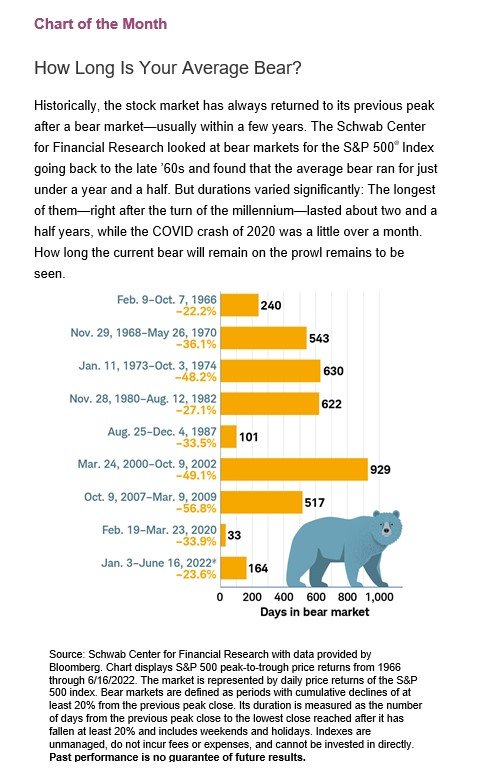

How Long Do Bear Markets Usually Last?

We are asking ourselves this question so you might be too. The answer is “too long” of course.

We like this chart from Schwab which provides a historical perspective, which of course means nothing about the current situation – except that bear markets have ended 100% of the time they have happened in the past!

Two More Inflation Fighting Ideas

After you have purchased I Bonds (you can still do, and we can help!) we want to share two more ideas!

Stock up on stamps and run low on gasoline. We are…