Bernie’s Blog

It’s Wedding Season at LFS: Part 2

Congratulations to Jordan and Matt, Lori and Charles, and Grandmother Toby! Photos from last weekend’s beautiful event in Orange, Virginia are attached.

We are so happy to welcome Matt to our family!

What is the VIX?

For those of you who unfortunately checked up on your portfolio on Monday August 5 when the S&P 500 dropped 160 points, you may still be asking yourself (and us) what actually happened that day.

Of course, no one really knows the actual answer, but it was likely a “perfect storm” of financial and non-financial events. The good news is that the market drop was short-lived (at least for this market cycle) and the S&P 500 quickly returned to its record-breaking highs (again for this market cycle)

If you dug a little deeper that day, you may have read about a massive spike in the VIX so we decided to dig a little deeper into what the VIX is and what it MIGHT mean, so we all know when it happens again.

First of all, the VIX is the ticker for the CBOE (Chicago Board Options Exchange) Volatility Index. The VIX, which is also called the Fear Index, is a real-time measure of investors’ expectations for short- term price changes in the S&P 500. It is calculated from prices of short-term S&P Index options. The index is calculated for the following 30 days and then annualized for the following 12 months. Simply, the VIX measures how fast stock prices are expected to change. In general, when the VIX goes up, stocks prices fall (investor fear is higher) and when the VIX goes down, stock prices increase (investor fear is lower).

Experts suggest the following rules of thumb:

- When the VIX is between 0 and 12, investors should expect low volatility for the following 30 days

- When the VIX is between 13 and 19, investors should expect normal volatility for the following 30 days

- When the VIX is 20+, investors should expect higher than normal volatility for the following 30 days

The long-term average VIX reading is 21. The highest ever VIX to date was almost 83, which happened in March 2020. The second highest reading was 81 which occurred during the 2008 financial crisis. On the

other hand, the lowest VIX recorded was 9 in November of 2017? Remember that? No one does.

So what happened to the VIX in early August?

The VIX spiked above 60, with the highest ever intra-day jump, and ended very close to the “market panic” level. Within just a few days, the VIX returned to a more normal level. Experts believe there were likely several factors for the spike:

- Concerns about the U.S. economy following July inflation and unemployment numbers

- Any excuse to sell, given the rapid rise in technology mega cap stocks tied to big bets in AI

- The steep decline in the Yen carry trade (investors borrowing Yen at very low interest rates and the purchasing U.S. or other assets with potentially much higher returns)

- Nuances in calculations

- World events – continuing escalation of mid-east wars, upcoming U.S. elections, China economic woes, etc.

The VIX today is 15.8. September has historically been the most volatile month of the year and the VIX has risen slightly for the last 30 days. Most of us expect ongoing market volatility for at least the next 40 days as the U.S. election nears so the VIX is a good way to see if other investors agree.

It’s WEDDING SEASON at LFS – Part 1!

Congratulations to Bradley and Maayan, Marci and Howard, and Linder grandparents. Photos from beautiful ceremony in Providence, Rhode Island are attached.

We are so happy to welcome Maayan to our family! Marci and Howard are grateful to all of you for the notes and texts – they will be back in touch soon!

The Financial Impact of the Olympic Games

As I am enjoying a much-needed replacement of my usual non-stop news coverage with Olympic swimming, skateboarding and soccer, I can’t help but wonder if anyone makes any money from all of this. Interesting question with the expected answer, which I am sharing below.

The answer is not really.

Historically, the average $10 billion needed to host the summer games has dealt a financial and environmental blow to the host city/country. The construction of temporary infrastructure, promised to aid the host city for the following decades, has rarely delivered on that commitment. The likely cost overruns, coupled with the potential environmental impact, has made it increasingly difficult to convince cities and countries to host these games. The notable exception to the negative financial impact was the 1984 Summer Games in Los Angeles, which delivered a $200 million surplus, largely by using existing infrastructure and offering valuable sponsorships and broadcast rights. Los Angeles will again host the summer Olympics in 2028, although some of the events will be held as far away as Oklahoma City! I will say that financial considerations aside, we really enjoyed the 1996 Summer Olympics here in Atlanta!

Now what about 2024 host city Paris? The International Olympic Committee (IOC) and Paris hope to reverse both the negative press and the historically negative financial and environmental trends. These are valiant efforts for sure but it’s way too early to assess the results. Critics insist that changing the financial and environmental trajectory will require a vastly different athlete and fan experience, with the likely need for permanent or a small rotation of host cities/countries. Since that’s not happening for the foreseeable future, let’s have a look at some of the numbers.

- 5 of the last 6 Olympic games have had cost overruns of at least 100%. And experts claim that some of the actual costs have not been included in the analyses. Many of the eventual host countries also invested $100 million in their bids to secure the Games.

- Summer Olympic games are almost double the cost of winter Olympic games.

- The current cost estimate for the Paris Olympic and Paralympic Games is $9.7 billion which is 25% over the initial bid from 7 years ago. Officials cite this little factor called inflation. Yep.

- Paris already had many sports venues so the plan was to limit new construction to the Olympic Village which will presumably become mixed-income housing later, an aquatics venue and a small arena. Not included in the $9.7 billion estimate was the $1.5 Billion to make the Seine clean enough to swim in, because presumably that was to be done regardless. Still remains to be seen how that will work out.

- There have already been 8.6 million tickets sold for the events in France (not sure if that includes tickets for the surfing in Tahiti) but early reports suggest fewer than expected visitors – with the expected negative impact on airlines, hotels, and restaurants. Paris is also apparently considered a prime tourist destination, so a long- term tourism boost is less likely.

My conclusion – I sure love to watch these events, even though I still cannot understand rugby, but not sure there is a strong financial proposition here. Happy viewing!

Elections and the Stock Market – no politics, just fun…

As promised, it’s time for some data and fun historical facts on the stock market before and after a Presidential election. This is a politics-free zone, so read on!

Let’s look first at what has historically happened to the stock market during Presidential election years and then what happens after the election, depending on which party wins. Spoiler alert….. it doesn’t really matter.

Now here is a shocker, election years tend to be volatile but in general, the market goes up. Remember though that there have only been 18 Presidential election years since 1952 so there is limited data. And let’s remember that in general over time, markets go up or none of us would be doing this. The S&P 500 has averaged a 7% gain in the election years since 1952 which is short of the 10% average gain in all years, but there has not been a down election year during this time. However, “re-election” years, which this clearly is, have delivered a better 12.2% gain since 1952. We all know that past market performance is no guarantee, but I like our odds given the performance already this year.

Now for some interesting election year data:

- Top sectors in presidential election years since 1952: energy and financial services

- Bottom sectors in presidential election years since 1952: materials and technology (hm?)

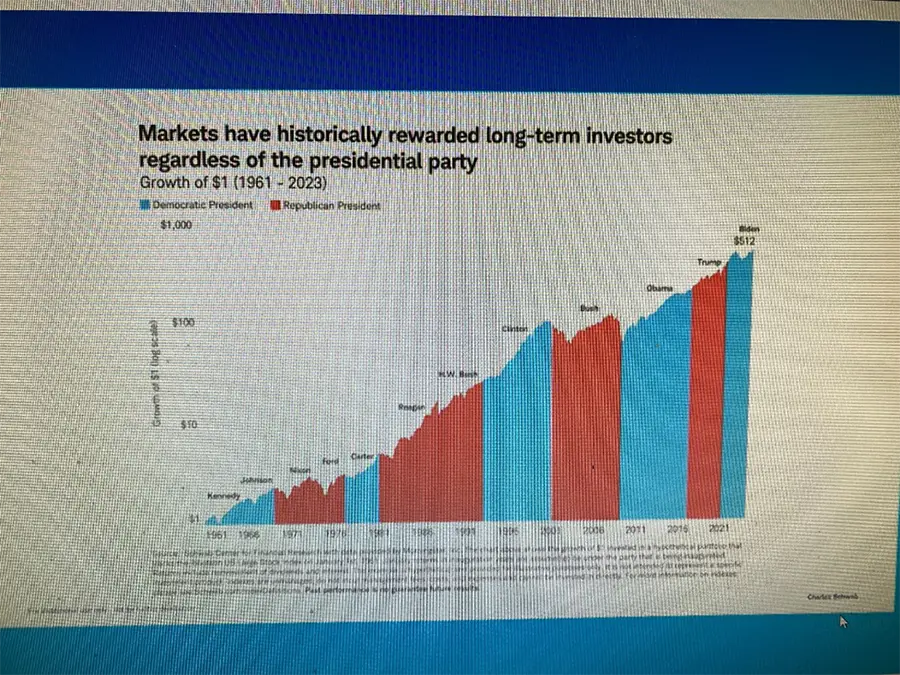

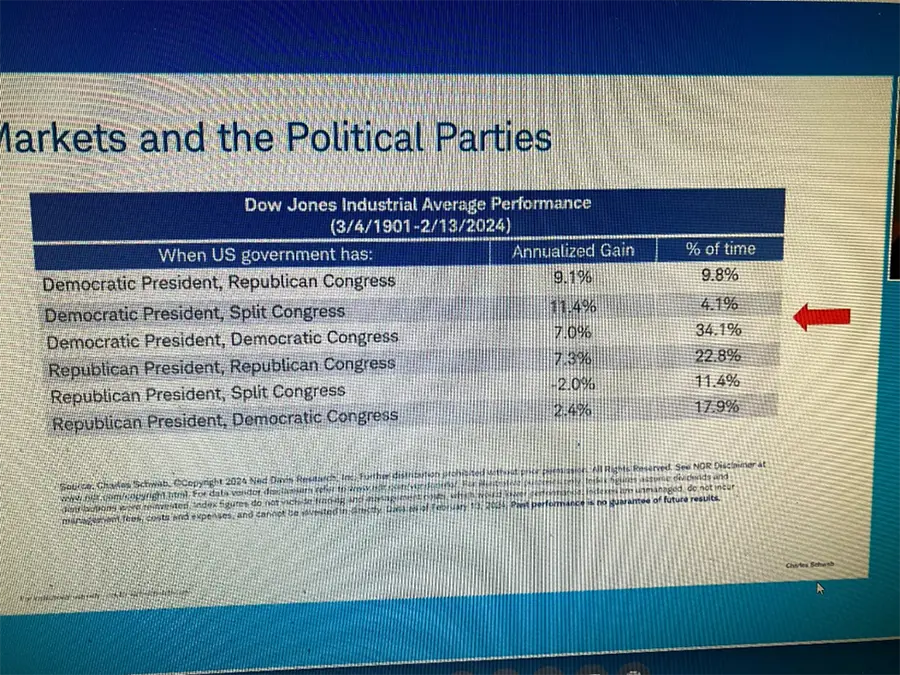

Now what happens after the election? In general, markets go up, regardless of which party wins the White House. And although I love the Schwab chart below which shows the market performance depending on the party of the President and Congress, my conclusion is that there is really no conclusion – in other words, there are other far more important factors which influence what the market does. But might be good Independence Day, Labor Day, and Thanksgiving party conversations anyway!

Linder Financial Services Named “Best of Alpharetta” for 6th Consecutive Year

FOR IMMEDIATE RELEASE

Linder Financial Services Receives 2024 Best of Alpharetta Award

Alpharetta Award Program Honors the Achievement

ALPHARETTA March 2024 — Linder Financial Services has been selected for the 2024 Best of Alpharetta Award in the Financial Advisor category by the Alpharetta Award Program.

Each year, the Alpharetta Award Program identifies companies that we believe have achieved exceptional marketing success in their local community and business category. These are local companies that enhance the positive image of small business through service to their customers and our community. These exceptional companies help make the Alpharetta area a great place to live, work and play.

Various sources of information were gathered and analyzed to choose the winners in each category. The 2024 Alpharetta Award Program focuses on quality, not quantity. Winners are determined based on the information gathered both internally by the Alpharetta Award Program and data provided by third parties.

About Alpharetta Award Program

The Alpharetta Award Program is an annual awards program honoring the achievements and accomplishments of local businesses throughout the Alpharetta area. Recognition is given to those companies that have shown the ability to use their best practices and implemented programs to generate competitive advantages and long-term value.

The Alpharetta Award Program was established to recognize the best of local businesses in our community. Our organization works exclusively with local business owners, trade groups, professional associations and other business advertising and marketing groups. Our mission is to recognize the small business community’s contributions to the U.S. economy.

SOURCE: Alpharetta Award Program