Bernie’s Blog

The CARES Act: Part 1

We hope all of you are healthy and at home as we begin the month of April. We are all working from home so don’t hesitate to continue to reach out!

We are all starting to study the new CARES Act so we want share what we have uncovered thus far. We have labelled this post as Part 1 because we are sure there will be more to come on this topic but let’s get started!

First of all CARES stands for Coronavirus Aid, Relief and Economic Security Act. The bill itself is over 800 pages long and has economic provisions for individuals, small and large businesses, state and local governments, public health and education/other.

There are implications for RETIREMENT PLANS which we want to summarize for you. These pieces apply to all, regardless of whether you have been impacted directly by the virus. There are other components of the Act which apply at this point only to those directly impacted.

RMDs (Required Minimum Distributions) have been suspended for 2020:

- This suspension includes inherited IRA’s

- There will be no penalty assessed if the distribution is eliminated in 2020

- Obviously the majority of retirees need this money for living expenses and will need to take the 2020 distribution anyway

If you have already taken your 2020 RMD, but don’t need the cash for living expenses in 2020:

- You have 60 days to return the dollars to a retirement account without paying the taxes

- We are not yet sure how Ameritrade will want to handle this transaction so let us know if you are interested in pursuing

- You can also convert this distribution to a Roth IRA and pay the taxes as you had planned. Again, call us if you are interested in doing this.

For those of you who aren’t subject to RMDs, but might want to take advantage of provisions in the CARES Act:

- The deadline for making 2019 contributions to an IRA of any type has been extended to July 15, 2020 to coincide with the federal tax filing deadline extension. We need to ensure that the contributions gets coded to the correct year so let us know if you want to do.

- Roth IRA Conversions are “on sale” right now. This is a great long term strategy for those of you who have traditional IRA’s and some cash. In short, if you convert a traditional IRA to a Roth IRA this year, you pay the taxes on the full amount you are converting in 2020, but then the Roth grows completely tax free forever – for you or your heirs. You can convert as much or as little as you would like so let us know if you want to discuss.

There are more provisions for additional distributions from IRA’s and loans/distributions from 401K’s. At this point, these pieces require proof of direct impact from the virus, including job loss. We can help work through these options with you if needed.

Again, most important thing is to stay healthy! We are here!

First Things First

As we all begin another chaotic week, we all know that your health and the health of all people around the world is far more important than the stock market, so let’s focus on that first. Once that is taken care of, the market will hopefully regain its health too.

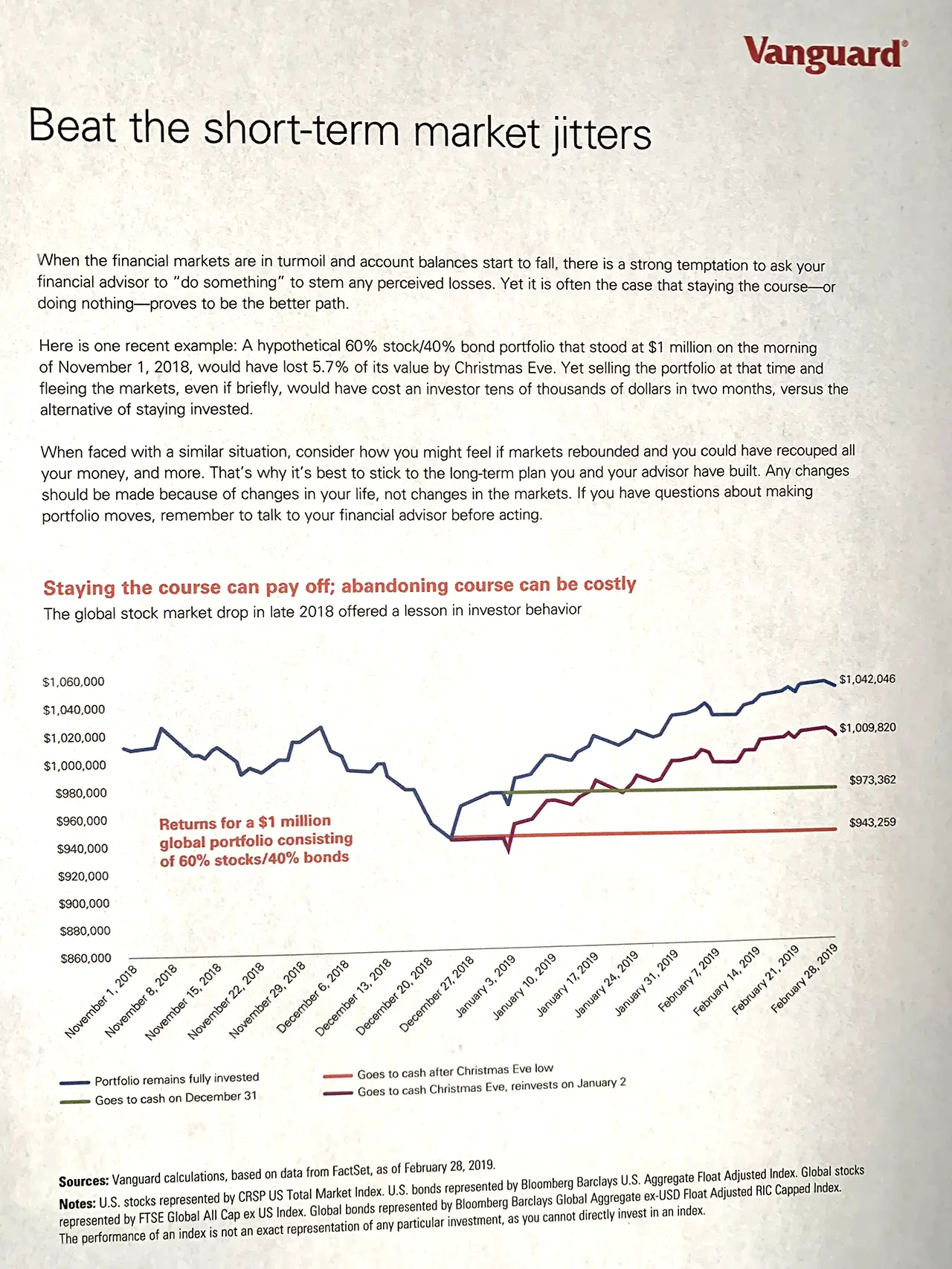

When you are ready for a distraction, we like this article from Vanguard which talks about the value of “staying the course” through market downturns.

But we also know it’s easy to say and hard to do!

We are here for you so if you are nervous or just want to catch up, don’t hesitate to call!

Market Uncertainty

Dear Clients,

As the new week and new month begin, we want to reach out to all of you who may be concerned about both your physical and financial well-being.

At this point, there is a tremendous amount of uncertainty regarding the spread of Coronavirus, the severity of the outbreak, and the duration. We are all relying on the expertise of the scientific and medical communities and we are fortunate that they are some of our country’s best and brightest.

The financial implications are also a huge unknown. While market corrections are inevitable, the speed at which this one occurred is dizzying, and there may well be more to come. The world has benefited from a global economy in which trade, travel, manufacturing, and research are shared across borders and oceans. The difficulty in containing a virus of this type is an obvious downside and the impact has grown as our economies have become more interdependent.

Concern about your investments is normal and expected. This situation is obviously particularly disconcerting because there is no financial, legislative, or political solution. Our advice during this time though, is the same as it has been during prior corrections. We do not recommend making changes to a portfolio based on fear, no matter how well justified that fear may be. Our view has been and remains that a long-term, well diversified portfolio will provide stronger returns over time, than attempting to time the market in response to the latest headlines.

That all being said, a reminder to all of you that we are here for you. If you want to talk about your specific concerns, please call or email, or come by the offices.

Marci, Lori, Tim, and Bernie

Two New Technology Options for You

We are happy to do introduce two new technology options which are designed to reduce paper, postage and time. Both of these upgrades are completely optional for you, but if you want to take advantage of them, let’s do it!

DocuSign

This functionality allows online form completion and signatures for nearly all Ameritrade documents. One downside of this option is that you will get an email link from Ameritrade – and that email link looks a lot like those “phishing email links” we have talked about before. We will let you know if we are sending you a document using DocuSign so that you can be on the lookout. After you electronically complete and “sign” the form, everything is automatically transmitted to Ameritrade and we get an email alert. Another downside is that mandatory attachments are messy or impossible. We are still working on making this piece easier.

What this means for you is that there are now three ways to complete and sign all the required paperwork:

- DocuSign (which we will not use unless you have agreed) – fastest and lowest carbon footprint!

- Print at LFS, mail to you and have you mail to Ameritrade or back to LFS – slowest and highest carbon footprint!

- Email form to you, have you print and complete/sign and then scan back to us. (Not all Ameritrade forms can be handled this way)

We are happy to use whichever method is easiest for you at the time.

AdvisorClient screen sharing

This functionality, which is brand new for advisors and clients, allows you to share most of your AdvisorClient screens with us (or Ameritrade) so that we can more easily answer questions and troubleshoot any issues.

This feature is simple to use:

- Log into NEW AdvisorClient

- Select “screen share” from bottom right of any page (green button)

- Give us or Ameritrade the “code for my agent” which is found at the bottom center of the page.

As always, let us know if you have any questions or concerns.

Exciting News from Linder Financial Services

It is with great pleasure that we announce Tim Kriegel as the newest member of our Linder Financial Services team! Tim has recently received his Registered Investment Advisor certification and will be soon getting to know you and our business.

Some of you may know Tim. He has been a long time LFS client and a former neighbor of Bernie and Toby in Hendersonville. He recently retired from his position at Selee Corporation where he held a number of executive financial positions, including Chief Financial Officer. He holds a B.S. in Business Administration from Clarion State University and is a Certified Public Accountant. He currently resides in Hendersonville.

We are so excited that Tim has agreed to join us. He will have two immediate priorities as he comes aboard:

- Tim will provide additional LFS financial advisory capacity in western NC and cement our long term commitment to that area which we all love so much. We will now be able to take on new clients in western NC and provide additional operational support to those of you that reside there now. But no worries, Bernie still thinks he’s in charge and is available for coffee and advice as always. You will continue to interact with him, and with us from Atlanta, just as you do now. But feel free to refer your friends and neighbors to us now – we can now absolutely support them and we are always truly grateful for your kind words to your friends and family.

- The new SECURE Act (see Bernie’s Blog) has reinforced the importance of smart generational wealth transfer so Tim will be leading our efforts to develop the “what” and “how “ to do this very important work with and for you. This work is not just paperwork, although there is always plenty of that. We are looking forward to building robust plans to get to know your heirs and build their trust in us, while we give you one less thing to worry about!

We are looking forward to introducing you to Tim over the next several months. Those of you in western NC will get to meet him in person sooner, but expect that all of you will hear from him over time. Please join us in welcoming Tim to Linder Financial Services.

Tim’s contact info:

Phone: 828-606-9078

Email: Tim.Kriegel@linderfinancial.com

Happy New Year Again: Retirement Plan Guidelines for 2020 (Part 2)

This blog will focus on the major 2020 changes to distributions from retirement accounts. The last blog entry focused on the 2020 changes to contributions to retirement accounts so feel free to look back to refresh your memory.

You may have heard of the new SECURE Act which was signed into law on December 20, 2019. We know you will feel more secure to know that “SECURE” is an acronym for “Setting Every Community Up for Retirement Enhancement Act”. The government has been busy with other priorities since December 20, so many of your usual information sources, including us, have not been fully updated yet. In truth, the government officials have not all yet agreed on some of the technicalities so just call us with questions and we will work through the implications individually with you as needed.

Required Minimum Distributions (RMDs)

- Participants will now be able to delay taking RMDs from their traditional IRAs until they reach age 72 (up from age 70 ½). This change only applies to those who turn 70 ½ in 2020 or later. If this applies to you, we have talked with you about it. If you are already taking RMDs, you must continue even if you are not yet 72. This is a good thing for most of us!

Inherited Retirement Accounts

- Beneficiary IRAs (non-spousal) must now be completely distributed within 10 years (instead of over the lifetime of the beneficiary). The rules for distribution to a spouse have not changed – the distributions are treated as if the IRA belonged to the spouse all along. Note that this means that all the income taxes must now be paid within 10 years. This is a massive, and largely unfavorable, change for most of us.

- Roth (non-spousal) Beneficiary IRAs must now also be distributed within 10 years, but there is of course no income tax due.

- This change might make a Roth IRA conversion more attractive as an estate planning strategy. We will discuss with you if applicable.

Adoption/Birth Expenses

- Penalty-free withdrawals from traditional retirement plans are now allowed for birth or adoption expenses, up to certain limits. Taxes must be paid on the withdrawals.