Bernie’s Blog

Is Anyone Else Often Baffled by the “Technology Ecosystem?”

As headlines continue to tout technology as one of the key drivers of economic growth now and in the future, we find ourselves wondering just what this technology ecosystem really is, how the pieces fit together and which companies participate in which part of this world. Since we are asking, we expect some of you are too.

The simplest explanation we found suggests that the technology industry is a pyramid. The growth prospects for each of these components can be different. See summary table below.

- The foundation is made up of companies which design and manufacture computer processing and memory chips.

- These are semi-conductor and computer chip firms.

- Computer chips are tiny pieces of semiconductor material.

- The next layer is companies which build devices and equipment of all types.

- These firms build the machinery needed to produce the semiconductors and the chips.

- Next are the actual device manufacturers.

- The devices are the pieces we use, like our Smartphones and computers.

- Networking/infrastructure is next layer.

- Next are computing cloud providers.

- These companies have massive data centers and rent computing power to businesses.

- There is a separate layer just for AI platforms

- The next layer has software companies.

- These run on the hardware and cloud infrastructure layers.

- And at the top are the cybersecurity companies which protect the networks and data.

Layer What These Companies Do Representative Public Companies Industry Growth Outlook AI & Processing Chips Perform AI calculations and computing tasks NVIDIA, Advanced Micro Devices, Broadcom Very Strong Memory Chips Store data used by computers and AI systems Micron Technology, Samsung Electronics, SK Hynix Strong Semiconductor Equipment Build the tools used to manufacture chips ASML, Applied Materials, Lam Research, KLA Corporation Very Strong Hardware & Devices Build computers, phones, and servers Apple, Dell Technologies, HP Inc. Moderate Networking & Infrastructure Connect data centers and businesses Cisco Systems, Arista Networks, Juniper Networks Moderate to Strong Cloud Computing Rent computing power and storage Microsoft, Amazon, Alphabet Strong Foundation Models (AI Platforms) Build AI and monetize (large language) models Anthropic, OpenAI, xAI, Google DeepMind, Meta AI Strong Software Create applications used by businesses and consumers Oracle, Salesforce, Adobe, ServiceNow Strong Cybersecurity Protect networks and data Palo Alto Networks, CrowdStrike, Fortinet, Zscaler Strong The technology ecosystem framework shown above is adapted from commonly used industry classifications and research published by MSCI/S&P GICS, Gartner, IDC, and the Semiconductor Industry Association. Company examples are illustrative and not recommendations.

What About Growth?

The biggest growth driver is artificial intelligence. AI requires advanced chips and massive data centers which has increased demand for semiconductor companies, chip manufacturers, chip equipment makers, AI platforms and cloud providers. Cybersecurity is also benefitting as companies become more digital. On the other hand, computers, smartphones, and basic networking equipment are likely to be slower growing areas.

Linder Financial Services is a dba of Thayer Partners LLC, (“Thayer”). Thayer is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Thayer by the SEC nor does it indicate that Thayer has attained a particular level of skill or ability. This material prepared by Thayer is for informational purposes only. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed by Thayer are based on economic or market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. Facts presented have been obtained from sources believed to be reliable. Thayer, however, cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. Thayer does not provide tax or legal advice, and nothing contained in these materials should be taken as tax or legal advice.

- The foundation is made up of companies which design and manufacture computer processing and memory chips.

Who is Kevin Warsh and Why Should We Care?

Kevin Warsh is the new Chairman of the Federal Reserve, replacing Jerome Powell. He served as a Governor on the Federal Reserve Board from 2006 through 2011, during the global financial crisis. Prior to his nomination to this position, he frequently commented on monetary policy and inflation. We are almost all old enough to remember when we didn’t even know the name of the Chairman of the Federal Reserve, much less have any idea what this person does.

The Federal Reserve has a dual mandate to promote maximum employment and maintain stable prices. Simultaneously. The tools the Fed has at its disposal are important, but limited to

- Setting the target for the federal funds rate (interest rate banks charge each other for overnight loans)

- Buying and selling U.S. Treasuries (and sometimes mortgage-backed securities) to manage the money supply

- Providing forward guidance, which is sometimes more influential than that actual Fed actions – particularly to the stock market

Although the Chairman sets the agenda for the meetings and shares information and decisions, the actual fed funds rate is decided by a vote of 12 members of the Federal Open Markets Committee which is a sub-set of the Federal Reserve. So, although the Chairman’s words are important, he does not set the rate.

Next, let’s talk about what has changed and why it matters now.

No doubt that this is a challenging time for the Fed. Inflation has been stubbornly above the Fed’s 2% long-term target while the unemployment rate has risen, although it is still well below historical averages. Energy prices, tariffs, and geopolitical tensions have complicated the situation, but economic growth has been surprising robust.

Some experts have predicted that Warsh will favor an aggressive rate cut schedule because President Trump appointed him, while other Fed watchers expect that Warsh’s strong historical focus on inflation will be reflected in fewer rate cuts for the foreseeable future, with a possible hike before the year is over. These fiscal hawks also believe that Warsh will push for a faster reduction in the Fed’s balance sheet/more aggressive sale of Treasuries which will reduce the money supply and slow economic growth, all in the name of inflation management. For us as average investors, this likely means “higher for longer” rates which puts downward pressure on growth stocks and longer duration bonds.

Adding additional uncertainty is the expectation that Chair Warsh will be less likely to signal future policy moves in advance (forward guide) than Chair Powell did. Those Wednesday afternoon press conferences after Fed meetings may no longer be “must watch” TV. The question might become which thing markets dislike more – uncertainty or negative signaling. We may find out. Either way, volatility in bond yields and equity pricing might increase.

As we step back here, history suggests that although Fed Chairs can create short-term market unease, long-term market performance is rarely tied to a single Fed official, chairman or otherwise. So as usual, we are recommending discipline and planning, rather than trying to predict rate cuts.

And now Wednesday afternoons after Fed Meetings are available on our calendars for you, instead of for Fed chair press conferences. Sounds like a win to us.

Linder Financial Services is a dba of Thayer Partners LLC, (“Thayer”). Thayer is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Thayer by the SEC nor does it indicate that Thayer has attained a particular level of skill or ability. This material prepared by Thayer is for informational purposes only. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed by Thayer are based on economic or market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. Facts presented have been obtained from sources believed to be reliable. Thayer, however, cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. Thayer does not provide tax or legal advice, and nothing contained in these materials should be taken as tax or legal advice.

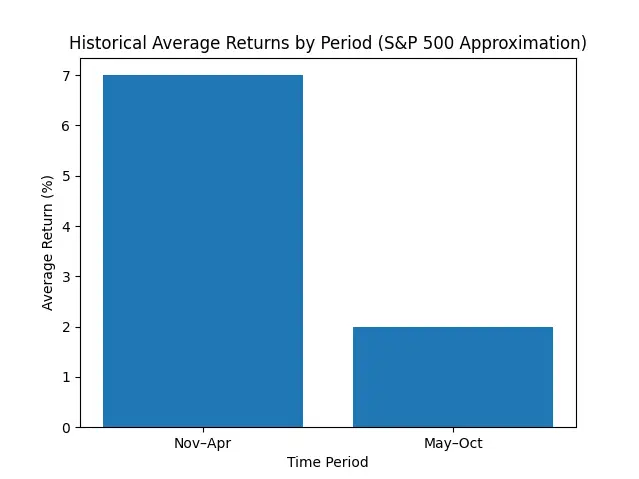

Where Did “Sell in May and Go Away” Come from?

Happy May! Happy Mother’s Day! Happy Graduation!

We have all surely heard this old “sell in May and go away” saying, but probably never dug into where it actually came from.

Actually, this strategy is based on the simple historical finding that says that over long periods of time, stocks tend to perform better from November through April than they do May through October. Although the reason why the returns are lower is not confirmed, experts have suggested that it is likely due to the historically lower summer trading volumes in the U.S. and Europe.

Whatever the cause, the data are interesting and might be good cocktail party talk.

Source: Historical S&P 500 total return data (multiple studies including Fidelity, Stock Trader’s Almanac, and long-term market research). Returns are averages and do not reflect any specific time period or guarantee future results.

Some of us might now be asking ourselves if we should sell in May and go away! It is not a surprise that we view this strategy as trying to time the market – which is something we don’t recommend. Trying to move in and out of the market based on a date on the calendar introduces two major challenges: when to sell and when to get back in. It’s hard enough to be right once, much less twice. We also know that sitting on the sidelines can mean missing the rebounds which can and do happen quickly. And many of these have happened in the summer months.

So instead of selling in May and going away, we recommend a mid-year look at your

- Life changes – but don’t assume they are bad. There are many terrific life changes too!

- Risk tolerance – are you pacing the floor at night? Tell us if you are.

- Financial plan and cash flows – we can update with new information and new scenarios easily. Let’s do if there are significant changes.

Linder Financial Services is a dba of Thayer Partners LLC, (“Thayer”). Thayer is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Thayer by the SEC nor does it indicate that Thayer has attained a particular level of skill or ability. This material prepared by Thayer is for informational purposes only. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed by Thayer are based on economic or market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. Facts presented have been obtained from sources believed to be reliable. Thayer, however, cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. Thayer does not provide tax or legal advice, and nothing contained in these materials should be taken as tax or legal advice.

Happy Financial Literacy Month

April is Financial Literacy Month – our favorite month of the year. Plus, we think everyone could use a bit of fun right now so it’s time for our annual financial literacy quiz.

When oil prices spike quickly and significantly, what is most likely to happen to the overall economy?

- Lower inflation

- Lower consumer spending

- Higher bond prices

- This is a dumb question because this will never happen

- No idea. I guess I need call LFS.

What happens to the cost basis of most inherited assets and why should I care?

-

- It stays the same as the original purchase price. My heirs will pay the same income tax I would pay if I sold.

- It resets to $0 so my heirs will pay taxes on the entire amount, not just the gain like I would pay

- It “steps up” to whatever the market value on my date of death so my heirs have no taxable capital gains at that time

- It is adjusted for inflation.

- No idea. I guess I need to call LFS.

When inflation rises unexpectedly, what usually happens to Treasury bond prices?

-

- Nothing

- They rise of course. That’s why I own them.

- They fall of course

- They become risk-free

- No idea. I guess I need to call LFS.

Which asset should I probably not transfer into my revocable trust during my lifetime?

-

- My Schwab brokerage/cash account

- My traditional IRA

- My primary residence

- My vacation home

- What is a revocable trust and why are we talking about it? I guess I need to call LFS.

What is my biggest long-term risk of holding too much cash?

-

- I will spend it

- My income taxes will go up

- My purchasing power will go down if there is inflation

- It’s harder to borrow money if I need it

- No idea. I guess I need to call LFS.

Linder Financial Services is a dba of Thayer Partners LLC, (“Thayer”). Thayer is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Thayer by the SEC nor does it indicate that Thayer has attained a particular level of skill or ability. This material prepared by Thayer is for informational purposes only. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed by Thayer are based on economic or market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. Facts presented have been obtained from sources believed to be reliable. Thayer, however, cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. Thayer does not provide tax or legal advice, and nothing contained in these materials should be taken as tax or legal advice.

Trump Baby Accounts: What Families and Grandparents Should Know

You have undoubtedly heard about new federally seeded investment accounts for children commonly referred to as Trump Baby Accounts. Regardless of politics, here’s what matters from a financial planning standpoint.

Spoiler alert – there are still some unknowns, and we expect the rules to change over the next 17 years.

What Are Trump Baby Accounts?

Trump Baby Accounts are proposed federally seeded investment accounts for children that may include:

- A $1,000 government deposit for eligible birth years (2025–2026). May be extended for future years.

- Up to $5,000 per year in contributions

- Tax-deferred growth

- Conversion to something similar to a traditional IRA at age 18. Might be possible to convert to a Roth IRA. Important details on both still being worked out, so stay tuned.

- Withdrawals taxed as ordinary income, most likely

- You can open these accounts for older children, but they will not receive the seed money

Who Benefits Most?

- Children born in 2025 or 2026 (eligible for seed money)

- Families wanting flexibility beyond education-only savings

- Grandparents looking for gifting opportunities (aren’t we all?)

Important Differences

Unlike a 529 plan:

- Withdrawals are not tax-free for education

- The child gains control at age 18

Unlike custodial accounts:

- Growth is tax-deferred

- Investment options may be more limited

Should You Open One?

If eligible, it likely makes sense to:

- Capture the government seed deposit of $1000. Some companies are also contributing on behalf of their employees.

- Coordinate contributions with 529 funding

- Consider the impact of control transferring at age 18. The child will likely pay taxes (at his/her rate) plus a 10% penalty if the funds are actually withdrawn at age 18, per the current plan. Subject to change.

Trump Baby Accounts are best viewed as a complementary planning tool — not a replacement for 529 plans or other strategies

How do we open a Trump Baby Account?

Once fully implemented:

- Confirm eligibility (U.S. citizen child with Social Security number)

- Open through a participating brokerage or financial institution, likely not before July. The custodian will guide you through the process to receive the seed money.

- If your child was born in 2025, you can start the process with your 2025 tax return via Form 4547, but you do not have to do it this way

- Fund annually (up to $5,000 in total from all family members)

- Invest according to program guidelines; most likely will be limited to an S&P Index 500 Fund

We expect major custodians to offer these accounts once final rules are in place.

As always, we are happy to help you work through the scenarios here.

Linder Financial Services is a dba of Thayer Partners LLC, (“Thayer”). Thayer is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Thayer by the SEC nor does it indicate that Thayer has attained a particular level of skill or ability. This material prepared by Thayer is for informational purposes only. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed by Thayer are based on economic or market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. Facts presented have been obtained from sources believed to be reliable. Thayer, however, cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. Thayer does not provide tax or legal advice, and nothing contained in these materials should be taken as tax or legal advice.

Welcome to the Two Newest Members of the LFS Family

We are so excited to welcome…

Eliana, daughter of Marci’s son Bradley and daughter-in-law Maayan, born in July 2025.

And

Cooper, son of Lori’s daughter Jordan and son-in law Matt, born in January 2026.

Everyone is doing great!